- India’s real estate market is complex, with strict regulations on property ownership.

- Land disputes are a major issue, accounting for 66% of civil cases and causing significant economic drain.

- Poor record-keeping and outdated land titles contribute to these disputes.

- The document proposes using blockchain technology and Verifiable Credentials (VCs) to create a more efficient, transparent, and secure system for managing land records and resolving disputes.

- Real estate tokenization is emerging as a solution, allowing fractional ownership and increased liquidity.

- A partnership between Rooba.Finance and Dhiway aims to combine asset tokenization and blockchain technology to innovate in this space.

The overall goal is to use technology to address India’s property-related legal and economic challenges.

The Indian real estate market is a unique one, governed by countless laws, regulations, and state-level amendments which control, and prohibit, the purchase of land by non-domiciled Indian residents. As a rough rule of thumb, foreign nationals who do not reside in India cannot have property registered in their names. PIOs and NRIs are restricted from buying agricultural, plantation, farm and other such land, though they are not prohibited from purchasing, selling or inheriting residential or commercial land save for one caveat – some states prohibit non-domiciled individuals from purchasing land of any type.

An indicative list of central laws that govern the purchase of land follows:

- Transfer of Property Act, 1882

- Registration Act, 1908

- Indian Stamp Act, 1899

- Real Estate (Regulation and Development) Act, 2016

- Benami Transactions (Prohibition) Act, 1988

- Foreign Exchange Management Act (FEMA), 1999

For NRIs to purchase residential property, the following documents are necessary:

- Passport and/or OCI Card

- PAN Card

- PoA registered for the specific transaction, if the NRI is not physically available for registration.

As regards agricultural land, all NRIs and PIOs are prohibited from purchasing it, though there is no bar on inheritance. However, in many states, even resident Indian citizens face restrictions relating to the purchase of land, or conversion of agricultural land to N.A. land by mutation.

The long and short of it is, that India makes it hard to buy real estate, makes you undergo stringent documentation and has, for all intents and purposes, a set of federal and state level laws in place to adapt to its diversity.

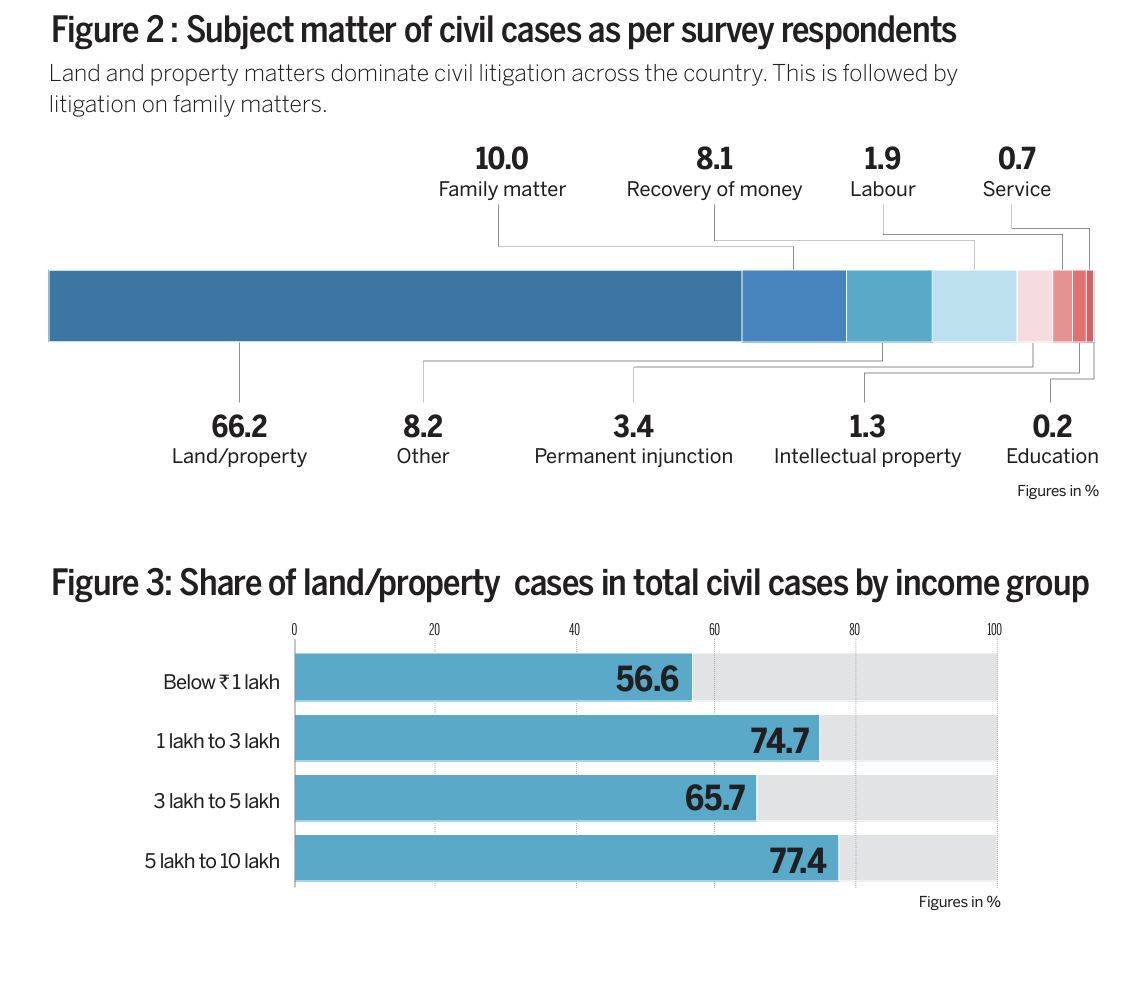

Despite this extensive legal system in place, an estimated 7.7 million people in India are affected by conflict over 2.5 million hectares of land, threatening investments worth more than Rs 14 lakh crore. Since land is central to India’s developmental trajectory, finding a solution to land conflict is a crucial policy challenge for the Indian government. Land disputes account for the largest set of cases in Indian courts – 25 percent of all cases decided by the Supreme Court involved land disputes, and surveys suggest that 66 per cent of all civil cases in India are related to land or property disputes. The average pendency of land acquisition cases, from creation to resolution in the Supreme Court, is 20 years on average. Some reports indicate that more than two-thirds of litigation pertains to property.

Data around Supreme Court (SC) cases is alarming. Cases pertaining to property that manage to reach the Apex Court at ‘Special Leave Petition’ or ‘Leave to Appeal’ stages are a mixed bag, ranging from land acquisition to conventional title disputes. To put it into perspective, the pecuniary jurisdictions of most states’ district courts have been raised to unlimited to ensure that High Courts do not get clogged by litigation. Up until 2015, litigants could approach High Courts directly to file property cases concerning properties over a certain value. Now, commercial disputes must all go to district courts at first, and require mandatory mediation in order to prevent lis (legal dispute) from being joined in the first place. Despite this, there is an alarming rate of litigation prevalent across all asset-value classes. This trigger-happy litigious mentality has ramifications beyond protracted pendency of cases. Individuals from lower socio-economic strata are unable to receive justice due to pendency in courts. Since they are unable to access quality legal advice, they often spend as long as 20 years or more litigating, generally on questions of title and devolvement of title. In principle, the Supreme Court must only deal with disputes concerning questions of law that have not been settled or require revisiting or interpretation. Broadly speaking, disputes with the highest incidence of percolating to the SC are Land Acquisition cases. By and large, as indicated by the figures above, 66% of all pending courts cases comprise property-related disputes, which can be bifurcated into private and against the state (land acquisition). Private disputes (between private parties, juristic or natural), can be further divided into those involving the title (competing title interests or encroachment) and those relating to devolvement (wills).

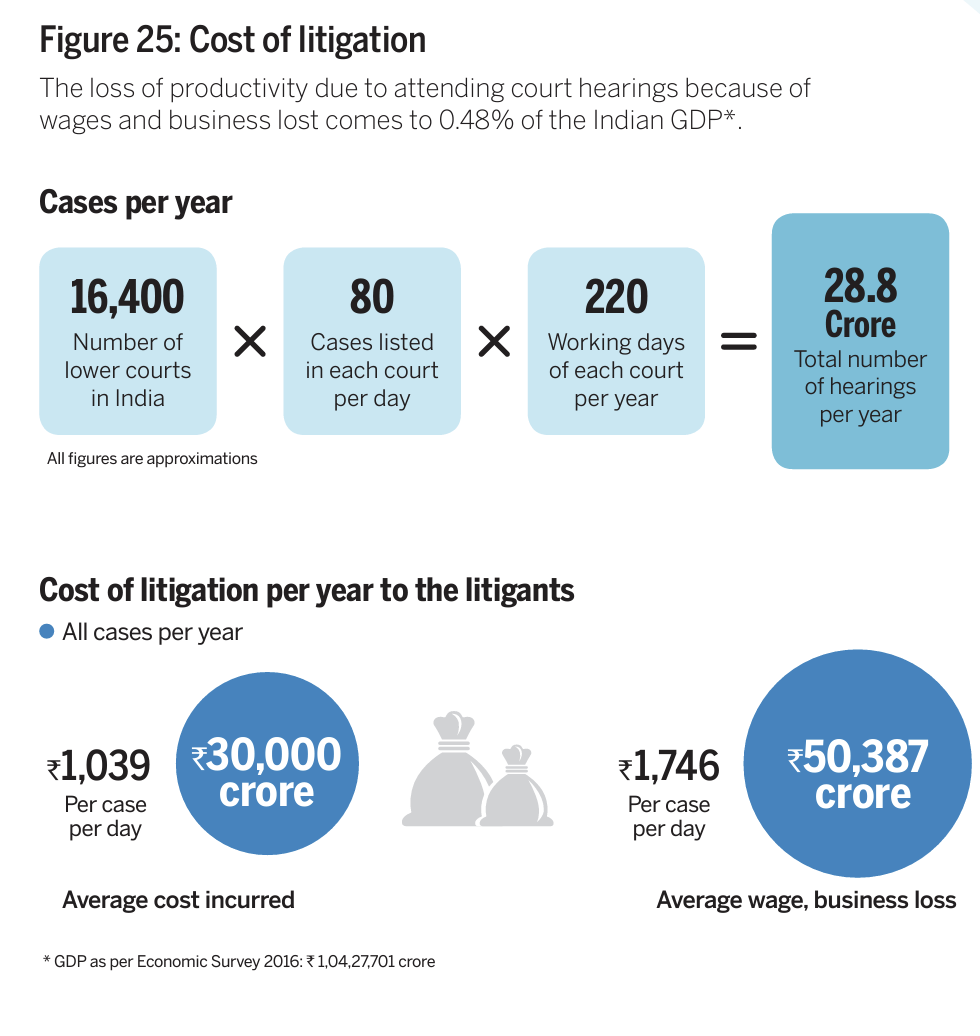

Cases which are not mediated or settled result in litigation, which has two economic outcomes. The first is that litigants lose money in hefty legal fees and the other is that the economy is detrimentally affected due to assets being locked in encumbrance. Without proposing some utopic litigation–free universe, what all can technology solve in such a status quo?

By 2040, real estate market will grow to Rs. 65,000 crore (US$ 9.30 billion) from Rs. 12,000 crore (US$ 1.72 billion) in 2019 and contribute 13% to the country’s GDP by 2025. Retail, hospitality, and commercial real estate are also growing significantly, providing the much-needed infrastructure for India’s growing needs. The problems at hand are economic drain to the people, a judicial strain to the infrastructure and is resulting in a lack of access to justice.

The solution? Verifiable provenance through digital records. Over the last decade, concerted efforts have been made to shift towards building and deploying Digital Public Infrastructure to solve the problems pertaining to data within India. Currently, the lack of trustworthy records accounts for a significant amount of litigation as well as the inability of government schemes to function. There are significant errors and discrepancies in the maintenance logs of land records. In a study conducted in Rajasthan, in 24 percent cases, the difference between the area on record and the area measured was more than 20 percent. To compound this, land titles are often considered presumptive, meaning that the person currently occupying the land is assumed to be its owner. The same study revealed that the state ceased maintaining records of land possession in 1972, and there is no data on land possession at the tehsil level. As a result, title records are frequently outdated; the registered owner might have died or sold the property without updating the records, making it challenging to determine current ownership.

Private disputes pertaining to joint ownership also take root in poor record-keeping. It gets particularly tricky when succession cases are instituted well into the future, sans any verifiable records. In India, devolvement follows religious or custom-based inheritance by default, unless expressly revoked by a will, thereby choosing testamentary succession (a quagmire of litigation in itself). All this has a detrimental impact on the ease of doing business rankings, specifically in respect of contract enforcement and property registration. India is currently ranked 163rd and 166th, respectively, on the abovementioned fronts. Both these factors, once again, are greatly affected by India’s persistent problem: an overwhelming number of land litigations.

In the early 90s, humanity was at the dawn of personal computing and the era of the internet. Juxtaposed to this groundbreaking advancement, India witnessed one of the largest scale financial frauds ever, the Harshad Mehta Scam. In this backdrop, the Securities and Exchange Board of India (SEBI) identified authenticity of securities as a paramount concern, and a hole to be plugged. By 1996, demat was mandated across public securities markets, ushering in an era of depositories, clearing corporations, registrar-cum-transfer agents and stock exchanges. SEBI used regulated intermediaries to ensure the safety and security of individuals participating in India’s securities markets.

Till date, some sectors of financial markets, such as private markets, have been left largely untouched by digitisation or dematerialisation. This has resulted in information asymmetry and data silos, culminating in opaque markets, inefficiencies in transactability and a lack of trust. At this juncture, we need to look towards innovative technology solutions to improve the sourcing, sharing and verification of data which assists the public in making financial decisions. At present, in 2024, we are witnessing increasing use cases of DLT and AI, and it seems only fitting that as we consider the evolving avatar of the internet, we must adopt and adapt or risk being mired in legacy market inefficiencies. In recent years, real estate tokenization has emerged as an unconventional investment option with advantages for both issuers and investors. The real estate sector now makes up about 40% of the digital securities market, amounting to approximately $200 million. Real estate tokenization typically turns a property’s value into a token that can be transferred and owned digitally by storing it on a blockchain. These fractional shares of ownership in the real estate are represented by these divisible tokens. A reliable database is necessary for private markets to become more liquid. Instead of being centralised, we think that this new database will be distributed and owner-controlled.

So, how does the Finternet Project and its contributors aim to solve this population-scale problem of verifiable data?

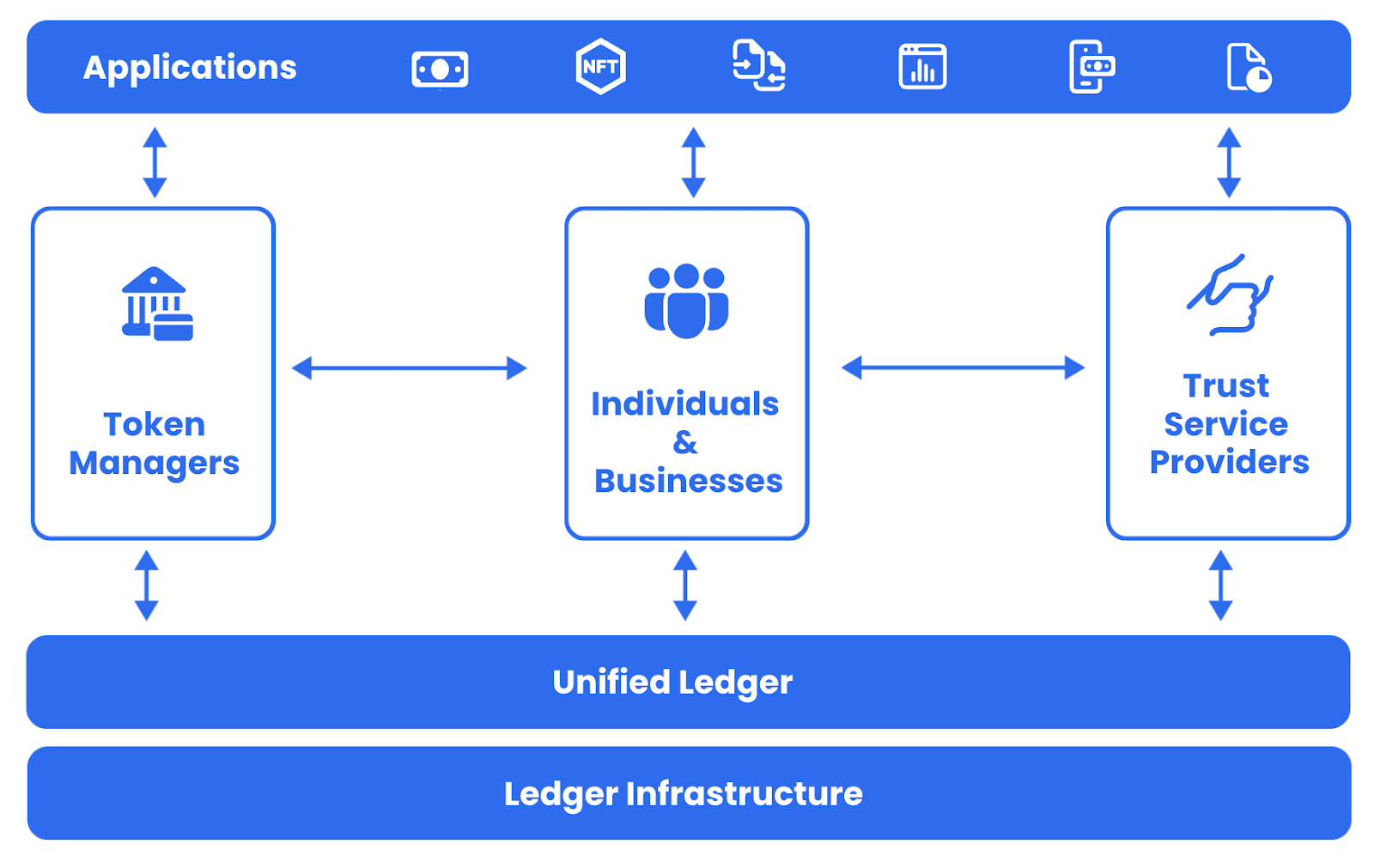

The vision of the Finternet is to build a set of rails for a user-centric ecosystem that unifies various fractured and siloed ecosystems using universal principles translated through technology. In the narrow compass of real estate, availability of authenticated data relating to property will unlock the hidden financial potential of a traditionally illiquid asset, remedying a major cause of litigation in India.

Verifiable Credentials

Finternet can revolutionise the administration and evidence process for dispute-resolution by integrating advanced digital tools and decentralised technologies. Through blockchain, it ensures that records and evidence are digitised and immutable, providing a reliable and tamper-proof source of truth. Verifiable Credentials (VCs) allow for instant authentication and verification of evidence, streamlining the process and ensuring authenticity. Real-time data access and transparency are enhanced, allowing for quicker decision-making.

VCs are digital certificates that can be used to prove the authenticity of information regarding an individual, organization or an asset. These credentials are stored securely and can be presented and verified in a decentralised manner, without the need for intermediaries. VCs are particularly useful in scenarios where trustworthiness is a priority, like in the case of property disputes.

In the context of property, verifiable credentials can be employed to:

- Authenticate Property Ownership: VCs can be issued by government authorities or trusted entities to certify ownership of a property. These credentials can be cryptographically verified by any party, ensuring that the ownership claim is legitimate and reducing the likelihood of fraudulent claims.

- Streamline Property Transfers: During property transfers, VCs can be used to verify the identities of the parties involved, as well as the authenticity of the property title. This can significantly reduce the time and cost associated with the transfer process, as it eliminates the need for extensive paperwork and third-party verification.

- Resolve Title Disputes: In cases where there is a dispute over property ownership, VCs can serve as tamper-proof evidence of ownership history. The use of VCs can expedite the resolution process by providing courts or arbitration bodies with a clear, verifiable record of ownership, thus reducing the duration and complexity of litigation.

- Improve Transactability: By using VCs, all parties involved in a property transaction can have access to verified and up-to-date information. This transparency helps in faster business decisions such as loans-against-property, home loans, credit decisions, etc.

- Integrate with Smart Contracts: VCs can be integrated with smart contracts to automate the execution of agreements based on verified conditions. For instance, a smart contract could automatically release payment upon the verification of a property transfer credential, ensuring that both parties fulfill their obligations.

By leveraging VCs within the property sector, India can move towards a more efficient, transparent and secure system of managing land records and resolving disputes. This technology has the potential to reduce the burden on the judiciary, minimise economic losses due to encumbered assets, and enhance the overall ease of doing business in the country.

Conclusion

The Indian real estate market faces significant challenges due to complex regulations, widespread land disputes, and outdated record-keeping systems. These issues result in economic inefficiencies, overburdened courts, and barriers to investment and development.

However, emerging technologies offer promising solutions to these long-standing problems. The integration of blockchain technology, Verifiable Credentials, and asset tokenization has the potential to revolutionize property management and transactions in India. By creating a more transparent, secure, and efficient system for recording and verifying property ownership, these innovations could:

- Reduce the number of property-related disputes

- Streamline property transfers and reduce associated costs

- Improve access to justice by providing clear, verifiable records

- Enhance the liquidity of real estate assets through tokenization

- Attract more investment to the real estate sector

The path forward involves continued development of these technologies, their integration into existing legal and administrative frameworks, and widespread adoption by stakeholders in the real estate sector. While challenges remain, the potential benefits of this technological revolution in property management are substantial and could transform India’s real estate landscape in the coming years.

Dhiway and Rooba alliance

Rooba.Finance and Dhiway are strategically collaborating to harness their respective strengths in asset tokenization and blockchain technology, driving innovation in the financial and property sectors. Rooba.Finance, with its expertise in asset tokenization, is pioneering the creation of digital representations of real-world assets, allowing for fractional ownership and enhanced liquidity in the market. Dhiway, a leader in blockchain-based infrastructure, provides the robust, secure, and transparent technology backbone necessary to support these digital assets. By integrating Dhiway’s advanced blockchain solutions, Rooba.Finance ensures that each tokenized asset is securely documented, traceable, and compliant with regulatory standards. This partnership not only facilitates the creation of new investment opportunities but also advances the secure and efficient management of digital assets, paving the way for a more decentralized and democratized financial ecosystem.